Publication date

Share this article

If you're comparing Qonto and iBanFirst, you're likely managing finances for a business with international operations.

Both platforms serve EU-based companies, but they're built for fundamentally different things. Qonto is a business banking platform with international payment capabilities. iBanFirst is a specialist cross-border payment provider and FX risk management platform.

Unlike comparisons where two platforms go head-to-head across every feature, Qonto and iBanFirst overlap in a few areas and diverge sharply in others. The question isn't just "which is better" — it's which one fits what your business actually needs.

So where do they compete, and where do they diverge?

Qonto overview

Qonto is a European business banking platform founded in 2017 that now serves 600,000+ businesses across eight EU markets, including France, Germany, Spain, Italy, and the Netherlands.

The platform centres on day-to-day operational finance: a EUR-based business account with physical and virtual business cards, expense management with multi-layer approval workflows, budget controls per team member, invoice generation in 29 currencies, automated receipt management, and integrations with 30+ accounting tools. The intuitive interface is a genuine strength.

Internationally, Qonto offers transfers to 150+ countries in 30+ currencies, powered by its partnership with Wise. Instant SEPA transfers are available for up to €100,000.

Qonto is a well-designed operational banking platform for day-to-day business finances (like budgets, invoices, cards, expenses). The international payment capabilities exist, but they're not the core strength.

iBanFirst overview

Founded in 2016, iBanFirst is an EU-based payment institution built for established SMBs operating across borders. We specialise in international payments and FX risk management, rather than general business banking.

In practice, that means a multi-currency account to hold and receive 25+ currencies (with local account details), cross-border payments in 135+ currencies to 180+ countries, real-time payment tracking with shareable links, FX risk management tools including three types of forward payment contracts, and dedicated human support from day one.

Our pricing model reflects this focus. There are no subscription tiers or setup fees, and exchange rate spreads are always transparent. Every customer gets the same tools, pricing, and support from day one.

iBanFirst vs Qonto at a glance

|

|

Qonto |

iBanFirst |

|

Core focus |

Business banking and expense management |

Cross-border payments and FX risk management |

|

Pricing model |

Tiered subscriptions (€49 – €249/mo for team plans) + FX conversion fees |

Custom spread set at onboarding — transparent rates across all transactions and currency pairs |

|

Currencies |

Hold and receive funds in 30+ currencies |

Hold and receive funds in 25 currencies |

|

International payments |

Cross-border payments in 30+ currencies to 150+ countries (via Wise partnership) |

Cross-border payments in 135+ currencies to 180+ countries |

|

FX risk management |

Not offered |

Fixed, flexible and dynamic forward payment contracts for all clients |

|

Dedicated support |

General support |

Support from FX experts for all clients from day one |

|

Payment tracking |

Standard tracking |

Timestamped updates at every step with shareable links for beneficiaries |

|

Expense management |

Cards, approvals, budgets, receipts |

Not offered |

iBanFirst and Qonto are more like adjacent platforms than direct substitutes for one another. Qonto is for managing day-to-day business finances, iBanFirst for cross-border payments and FX risk.

Where Qonto and iBanFirst overlap

Qonto and iBanFirst share common ground in a few areas — business accounts, international payments and multi-currency capabilities. The following sections cover that shared territory before moving to where each platform has its own distinct strengths.

Business account features beyond traditional banks

Both Qonto and iBanFirst are payment institutions — not traditional banks — and both offer business account capabilities that go beyond what standard bank accounts provide.

Both are regulated EU payment institutions (Qonto in France, iBanFirst in Belgium), both prioritise compliance and security, and both provide accounts designed for companies whose needs have grown past what traditional banking alone covers.

But "account" means something different at each platform.

- Qonto's business account is a full operational hub: EUR-denominated, with cards, expense management, budgets, and invoicing built in.

- iBanFirst offers a multi-currency account with 25+ currencies and local account details, built for receiving, holding, and sending in foreign currencies across cross-border B2B payments.

Neither platform is designed to replace your traditional bank account entirely. Both work as supplemental systems that expand what your financial toolkit can do. Qonto adds operational banking capabilities (cards, expenses, invoicing). iBanFirst adds cross-border payment depth and FX risk management.

You'll likely still have your traditional bank account. These platforms help expand what you can do with your funds (and how you manage them).

Multi-currency account capabilities

Both platforms handle multiple currencies, but the approach differs — and the distinction matters depending on how your business uses foreign currency day to day.

Qonto's account is EUR-based. You can send and receive payments in 30+ currencies through the Wise connection, but foreign currency received is automatically converted to EUR on arrival. If you receive a GBP payment, it lands as EUR in your account.

iBanFirst offers a true multi-currency account with 25+ currencies available. If you receive a GBP payment, you can choose to hold it in GBP until you want to convert — or use it to pay a GBP-denominated invoice directly. You can also collect international payments using local IBANs for each currency.

What's the practical impact?

For businesses that receive payments in foreign currencies or manage expenses across multiple currencies, auto-conversion means absorbing FX conversion costs on every inbound payment with no control over timing. A true multi-currency account lets you hold currencies strategically and convert when rates are favourable.

Qonto's approach is simpler — everything stays in EUR — and for businesses with primarily EUR-denominated operations, that simplicity is an advantage. For businesses with material foreign currency exposure, iBanFirst's approach gives more control over when and how conversions happen.

International payments

Both platforms can be used to send international payments, but the underlying infrastructure is fundamentally different.

Qonto offers international transfers to 130+ countries in 30+ currencies through a partnership with Wise Business. The capability works for routine transactions. Instant SEPA transfers go up to €100,000, and international transfer costs range from 0.56% to 1.8% per transfer depending on the currency, with a €5 minimum.

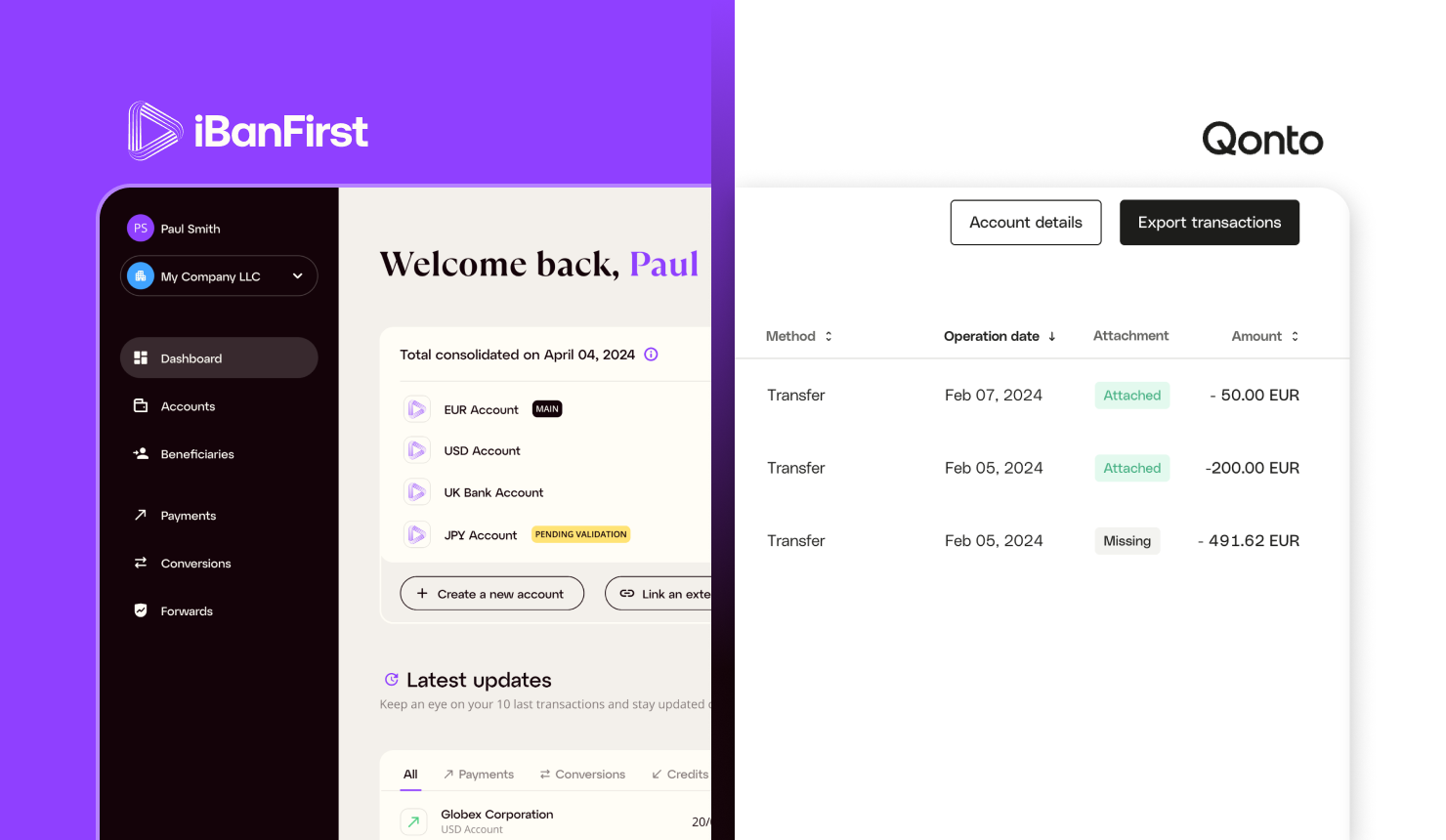

With iBanFirst, you can send cross-border payments to 135+ countries via an easy-to-use infrastructure — the platform manages the payment rails, controls pricing, and handles the full transaction lifecycle. Pricing is a transparent, standard exchange rate spread. Every SWIFT payment includes real-time tracking with timestamped updates and shareable tracking links, so you can send a supplier a link instead of fielding "where's my payment?" emails.

For businesses processing occasional international payments, the difference may be marginal. For businesses managing significant cross-border payment volumes — regular supplier payments, intercompany flows and international collections — the platform gives you more control over pricing, deeper feature depth and direct access to FX specialists who can support on execution timing for large or complex transactions. You can also pay suppliers abroad with full visibility into every step.

Both can send the payment. The question is whether cross-border payments are built-in or bolted-on, and how important that actually is for your day-to-day operations.

Where Qonto excels: Operational finance and day-to-day banking

Qonto's strengths lie in operational finance tools designed for day-to-day business management. These are real advantages for businesses that need them, but out of scope for what iBanFirst aims to be.

Expense management, cards and team spending controls

Expense management is what Qonto is built around, and it's a genuine advantage over any cross-border payment specialist.

The key capabilities: physical and virtual business cards with personalised spending rules per team member, multi-layer approval workflows for team collaboration on spending decisions, real-time notifications for every transaction, receipt capture and management with VAT detection, and sub-accounts for budget allocation across teams and projects.

For finance teams managing team spending, card expenses, and operational budgets, Qonto provides purpose-built tools that replace a combination of corporate cards, expense apps and manual spreadsheets.

On the flipside, iBanFirst doesn't offer cards, expense management or team spending controls because it's core focus is different. If your primary pain point is managing team expenses and operational spending, Qonto is built for that.

Invoicing and accounting software integration

Qonto goes deeper on invoicing and accounting integration than most platforms in this space, and it's a genuine strength.

The platform offers quote and invoice generation (one-off and recurring) in 29 currencies, automated invoice collection from Gmail and cloud storage, certified digital receipt management, and integrations with 30+ accounting software tools, plus an EBICS interface for automated bank feeds.

For businesses where invoicing and bookkeeping are significant operational activities, Qonto creates an integrated loop from invoice creation through payment receipt to accounting reconciliation, all in one platform.

iBanFirst integrates with most major accounting software and ERPs to automate payment workflows and offers an API for building custom integrations when your stack requires it.

Here's where the use cases differ:

- Qonto's integrations centre on invoicing, receipt management and bookkeeping automation.

- iBanFirst's integrations centre on cross-border payment workflows (including invoice payments), FX data sharing, and reconciliation for international transactions.

Both connect to the tools finance teams already use, but each focuses on what its platform is built for.

Where iBanFirst excels: Cross-border payments and FX risk management (with human support

Similarly, iBanFirst's strengths are in areas where Qonto isn’t primarily focused: FX risk management, cross-border payment infrastructure, and support from human specialists.

FX risk management and forward payment contracts

iBanFirst offers three types of forward payment contracts for managing currency risk:

- Fixed forward payment contracts: lock in today's exchange rate for a known future payment date and amount — best for businesses with predictable payment schedules

- Flexible forward payment contracts: lock in a rate for a set total amount, then draw down across multiple payments over time — best for businesses with known total exposure but variable payment timing

- Dynamic forward payment contracts: lock in a floor rate for downside protection while keeping upside if rates move in your favour — best for businesses that want protection without giving up potential gains

All three are accessible to every iBanFirst customer from day one with no minimum volumes, features gated behind premium tiers, or ramp-up period. Why does this matter for SMEs?

For businesses invoicing or paying in foreign currencies, exchange rate movements directly affect margins. A 2–3% rate swing on a €500,000 quarterly payment cycle is €10,000–€15,000 in unplanned cost. Forward payment contracts let you lock in rates and forecast costs with certainty — turning a variable cost into a known one.

Without these tools, every international payment is executed at the spot rate on the day of the transaction, with no way to lock future rates or manage currency exposure proactively.

Native cross-border infrastructure and dedicated FX support

Beyond FX risk management, iBanFirst's cross-border infrastructure is built in-house rather than outsourced. That means the platform handles every step of an international payment from initiation to delivery, giving you direct visibility and control over what's happening at each stage.

What native infrastructure means in practice:

- Payment tracking with real-time timestamped updates and shareable tracking links — send a link to a supplier so they can see exactly where their payment is, without back-and-forth emails

- Direct control over pricing with a standard exchange rate spread applied uniformly, not variable based on a third party's fee structure

- Deeper corridor coverage (135+ countries) with operational oversight of the entire payment chain

This matters most for businesses processing high volumes of international payments, where visibility and cost control compound over time.

On the support side, every iBanFirst customer gets a dedicated FX specialist account manager from day one — someone with market expertise who can advise on execution timing, forward payment contract strategy, and currency market context. This isn't general business banking support. It's specialist FX guidance.

For businesses where cross-border payments are a core operational function rather than an occasional need, native infrastructure and specialist support create advantages that compound over time.

How payment tracking works in iBanFirst

iBanFirst provides detailed payment tracking with timestamped updates at every step of the payment lifecycle, from initiation through settlement.

What sets it apart is the ability to share tracking links directly with suppliers or partners, so they can see payment statuses themselves. That effectively eliminates the "Where's my payment?" back-and-forth that eats up time for finance teams managing dozens or hundreds of international payments.

Why does this matter? It's not just about convenience. When your suppliers can check payment statuses without calling or emailing, your finance team gets that time back — and your supplier relationships benefit from the transparency.

iBanFirst's support model

iBanFirst provides dedicated account managers from day one. Every client gets access to specialists with real FX expertise. They help finance teams with execution timing, FX strategy and market context. They're not generic support agents reading from scripts.

Dedicated support isn't just about issue resolution either. When you're making FX decisions that directly affect your margins, having a real person who understands your business context makes a difference — especially when automated tools alone don't give you the full picture.

For businesses where FX decisions directly affect margins, that kind of accessible human expertise is a genuine operational advantage.

How to decide which platform is right for your business

iBanFirst and Qonto serve different primary needs — the right choice depends on what your business actually requires day to day.

Questions to ask before choosing

Before comparing features, start with your operational reality. The right platform depends on what you actually need.

- Is your primary pain point managing team expenses, cards, and operational budgets — or managing cross-border payments and FX exposure?

- Do you invoice and pay primarily in EUR, or do you regularly transact in multiple currencies?

- Do you need FX risk management tools like forward payment contracts to protect margins on foreign currency transactions?

- Is pricing transparency and predictability a priority — fixed exchange rate spreads vs tiered subscription costs?

- Do you need analytics and reporting on FX exposure, or on operational spending?

Your answers will point clearly toward one platform or the other — or reveal that you might benefit from both for different functions.

The narrower the overlap between these platforms, the clearer the decision becomes. It's about matching the tool to the job.

When Qonto may be the best fit

Qonto may be the best fit if:

- You need a modern business banking platform with cards, expense management, and team spending controls

- Your business operates primarily in EUR with occasional international payments

- Invoicing, receipt management, and accounting automation are daily operational needs

- You want to supplement your traditional bank with a more intuitive layer for day-to-day finances

- Your international payment volumes are modest and don't require specialist FX tools or dedicated FX support

When iBanFirst may be the best fit

iBanFirst may be the best fit if:

- You manage significant cross-border payment volumes — regular supplier payments, intercompany transfers, or international collections

- You need FX risk management tools like forward payment contracts to protect margins against currency movements

- You transact regularly in multiple currencies and need to hold, convert, and send in 25+ currencies from a single multi-currency account

- You want dedicated FX specialist support from day one, not general business banking support

- You value transparent, predictable pricing with no tiered subscriptions or variable fees based on plan level

- You've outgrown providers that treat cross-border payments as a secondary feature and need a platform where it's the core product

The two providers don't necessarily conflict, either. A business could legitimately use Qonto for operational banking and iBanFirst for cross-border payments and FX. They serve different functions with little overlap, so no redundancy. But if cross-border payments are a core operational need rather than an occasional transaction, iBanFirst is built for that specifically.

Start managing your cross-border payments with iBanFirst

With iBanFirst, you can:

- Hold and receive funds iin 25+ currencies from a single multi-currency account

- Make payments in 135+ currencies to 180+ countries

- Track every international payment with shareable, real-time tracking links

- Lock in exchange rates with forward payment contracts (fixed, flexible, or dynamic)

- Get direct access to FX specialists who understand your cross-border operations

Request an account today and see why thousands of international businesses choose iBanFirst.

Pricing and features referenced in this article were reviewed in 2026. We recommend verifying current details on each provider's website.

Topics