-1.jpg)

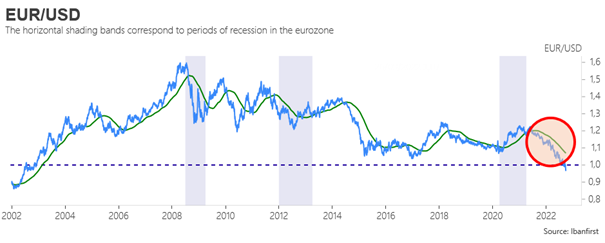

Since the start of the year, all the major currencies have dropped against the U.S. dollar, with the exception of three (the Russian ruble, the Brazilian real and the Mexican peso). The euro has decreased 15 % year-to-date. The depreciation has accelerated since the summer despite the beginning of a monetary tightening cycle in the eurozone (interest rate hike by 50 bp in July and by 75 bp in September). The money market now expects the European Central Bank will hike by another 75 bp in October. But this will not be enough to bring support to the euro. A fall of the euro to 0.90$ was unimaginable a few months ago. Now, it is a credible price target for year-end.

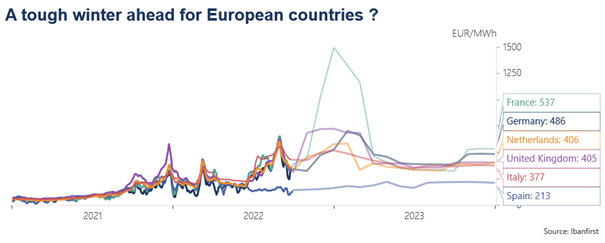

The European electricity market is breaking down. Wholesale electricity prices for several countries are close to €500 per megawatt hour (MWh). This is about ten times 2020 levels. While the surge is driven by rapidly rising gas prices due to the war in Ukraine, it also stems from problems with nuclear generation in France, where many power plants are offline for technical reasons. The European Central Bank can fight a recession or widespread inflation. But it is obviously powerless to fix the European electricity market. The next few months will be tough for consumers. Expect the energy crisis to drive economic weakness. Based on the latest PMI indicators, the eurozone has certainly already entered into a recession in the third quarter. This is a net negative for the euro, of course.

From a technical perspective, the EUR/USD cross is evolving well-below its 200-day moving average (green line). This is a strong signal indicating a continuation of the current downward trend. A few indicators show the euro is undervalued relative to the eurozone economic fundamentals. But in a momentum market, this matters little.

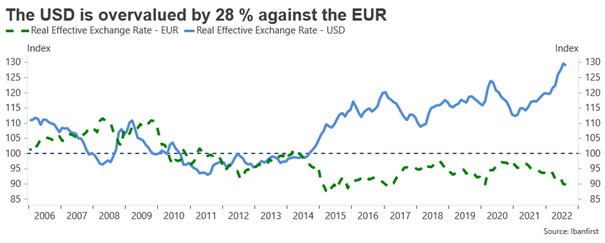

The U.S. dollar is 28 % too expensive against the euro based on the real effective exchange rate. This is the weighted average of the U.S. dollar against the currencies of the United States’ main trading partners. In theory, this is good news for the eurozone as this should boost exports. This is not the case, actually. A too weak euro leads to an increase in the prices of imported intermediate goods that are essential to the production process (energy, for example). This in fact reinforces the severity of the recession. The current U.S. dollar exchange rate is everyone’s problem. But we are not at levels of overvaluation that would provoke coordinated intervention by the United States, the eurozone, Japan and the United Kingdom, as we saw in the September 1985 Plaza accord. Therefore, expect the euro drop to continue, with a first short-term target at 0.96 which, if crossed, could open the door to a test of the psychological support area of 0.90 by year-end.