More businesses than ever are operating across borders, connecting with suppliers, clients, and partners worldwide.

But here's the million-dollar question: Are your international payments keeping up?

Whether you're an exporting company sourcing materials globally, an e-commerce business dealing with currency volatility, or a local company serving international clients, the way you handle cross-border payments can have a big impact. Inefficient systems could mean higher costs, delays, and added complexity.

Traditional banks have been the go-to for decades. They’re familiar, dependable, and part of what we’ve always known. But today, a new wave of fintech providers like iBanFirst, is redefining cross-border payments.

Which fits your business best?

This guide compares traditional banks and specialised providers, giving you the insights you need to make the best choice for your international payment needs.

Fine print to bottom line: hidden costs the banks won’t tell you

Cross-border payments seem simple, but the costs stack up fast. Each transaction takes a bite out of your profits. Most businesses don't realise how much they're really paying. Knowing the true fee structures of different providers isn't just helpful—it's essential for your bottom line. Are you confident you're not overpaying?

Exchange rates

The exchange rate applied to your transactions can have a significant impact on your overall costs. Traditional banks often apply a substantial markup to the interbank exchange rate, ranging from 4% to 6% or even higher.

Specialised providers, like iBanFirst, typically offer rates much closer to the interbank rate. Over time, these savings can be substantial, especially if you have a high volume of international transactions.

Transfer fees

Both banks and specialised providers typically charge a fee for processing transfers, but traditional banks often have high fixed fees that can make smaller transfers disproportionately expensive. For lower-value transactions, these set fees can eat up a significant portion of the total amount.

In contrast, fintech providers usually offer lower fees with more transparent pricing, often keeping fixed charges under 10 euros, making them a more cost-effective choice for frequent, smaller transfers.

Hidden costs

Traditional banks may charge additional fees like foreign exchange commission fees, account maintenance fees, or access to bank transfer messages. These fees aren’t always clearly communicated upfront.

Specialised providers like iBanFirst offer price transparency, with all fees clearly stated before you initiate a transfer.

Long-term cost implications

While individual transfer costs are important, businesses should also consider the long-term cost implications of their chosen payment solution. Traditional banks often require you to maintain high account balances or pay monthly fees for business accounts with international transfer capabilities.

Specialised providers typically have lower overhead costs and can offer more competitive pricing as a result.

Traditional banks have higher markups and less transparent fees. Specialised providers offer lower rates and crystal-clear cost structures.

The difference? Potentially thousands in savings.

Curious about your actual cost savings? Use our savings calculator to estimate how much you could save with iBanFirst cross-border payments.

Onboarding to payout: comparing processing speeds

Speed in financial transactions isn't just a nice-to-have—it's a critical business advantage.

Slow transfers have real consequences. They can delay crucial purchases, strain supplier relationships, and cause you to miss time-sensitive opportunities.

The speed of your money movement isn't just about efficiency—it's a key factor in your overall competitiveness and growth potential.

Onboarding and account setup

Traditional banks often involve a more time-consuming onboarding process, which may include:

- In-person visits to local branches

- Extended wait times on phone calls

- Submitting various physical documents

- Potential delays due to manual processing

These steps can stretch the onboarding process to several weeks or even months.

In contrast, iBanFirst and similar dedicated providers offer streamlined, all-digital onboarding:

- Fully online application process

- Digital document submission

This approach often reduces onboarding time to a matter of days.

Payment processing times

Traditional bank transfers, especially those using the SWIFT network, can take anywhere from 2 to 5 business days to settle.

In contrast, fintechs like iBanFirst have optimised their internal processes and built alternative networks and partnerships to speed up payments significantly. As a result, most transfers are completed in less than 2 days, with some transactions settled in as little as 1 hour through real-time gross settlement—or even instantly between iBanFirst accounts.

User experience: from legacy to leading-edge

For many years, traditional banks didn’t feel a strong need to invest heavily in technology. However, with the rise of innovative competitors offering faster, more cost-effective, and user-friendly cross-border payment solutions, banks have had to adapt.

While they’re modernising—some now offer international transfers through their online platforms—, their tech investments are spread thin, covering everything from personal accounts to loans.

As a result, banks struggle to match the agility and customisation of more specialised competitors, often missing the advanced features that dedicated cross-border providers offer.

Specialised providers and technology

From day one, cross-border payment providers like iBanFirst have leveraged technology to build their systems from the ground up, specifically addressing common pitfalls that businesses face with traditional banks. With their laser focus on cross-border payments, they offer more advanced features and a far more user-friendly experience.

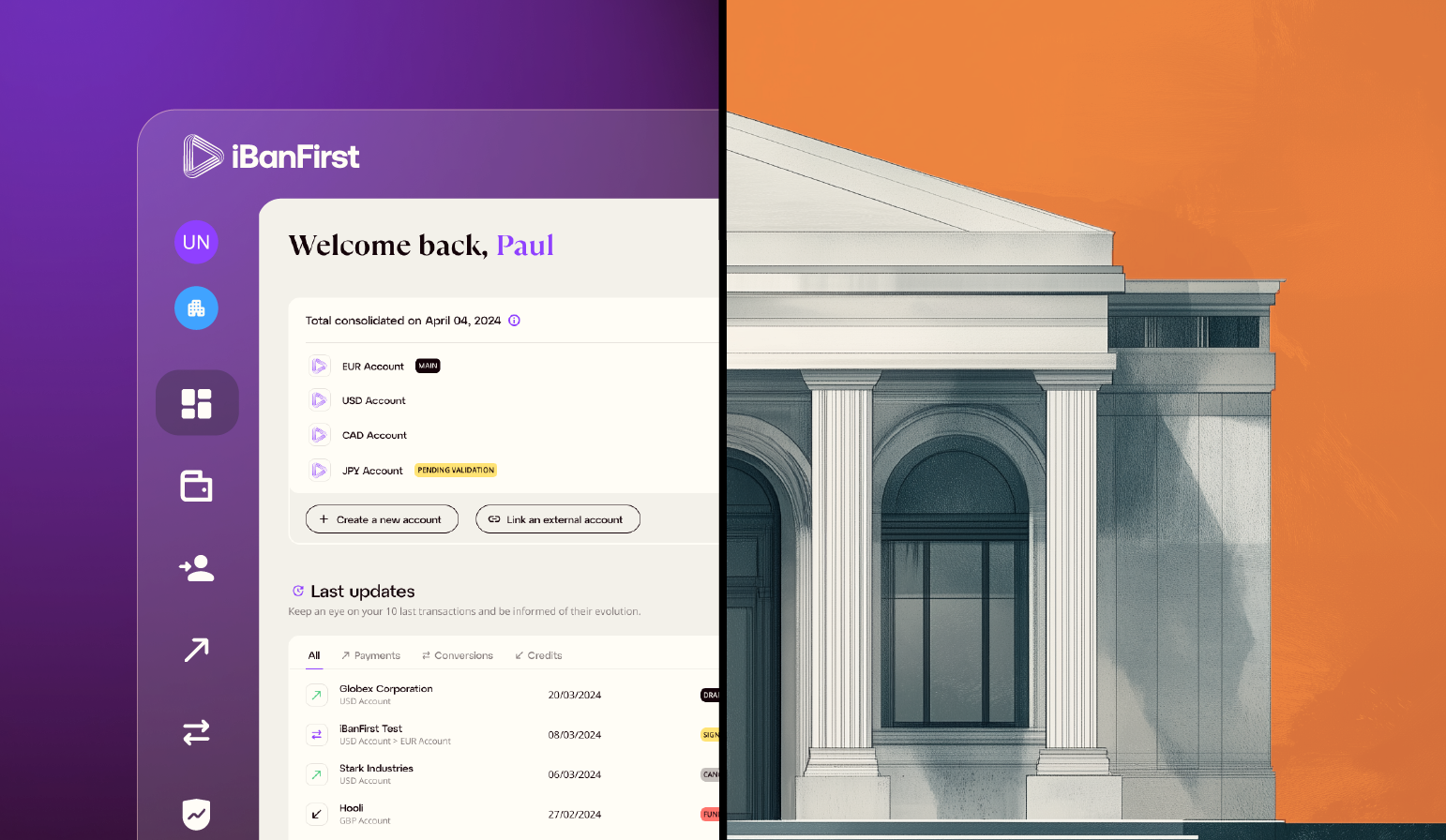

Thoughtful and easy-to-use platforms

Unlike traditional banks, cross-border payment providers offer advanced platforms that are accessible anytime, anywhere, allowing businesses to manage all their international transactions from a single interface. Designed with a consumer-grade user experience, these platforms make complex processes easy to navigate, enabling SMBs to handle multiple accounts, currencies, and both incoming and outgoing payments—all without the inconvenience of traditional systems.

Real-time market data

At the core of their offerings is real-time exchange rate data and currency conversion, for all users, not just the big enterprises. Users can access live, up-to-the-second exchange rates for a wide range of currency pairs and execute buy or sell orders instantly. Platforms like iBanFirst also offer historical rate charts to help inform decision-making.

FX alerts

.gif?width=700&height=340&name=FX-Alert-2-ezgif.com-optimize%20(1).gif)

Complementing this real-time data are sophisticated FX alerts and market order systems. Users can set up customizable alerts for when exchange rates reach specified levels, enabling them to capitalise on favourable market movements and never miss opportunities.

Payment tracking

![]()

Payment tracking features provide real-time tracking of payment status from initiation to receipt. You can see a detailed breakdown of all fees associated with each transaction, and share the payment tracker with beneficiaries.

Payment approval workflows

Payment approval workflows are another essential feature, offering customisable multi-level approval chains and thresholds that align with internal processes and add an extra layer of security for high-value transactions.

Risk management

Unlike traditional banks, which often reserve FX risk management products for large enterprises, many cross-border payment providers make these tools accessible to businesses of all sizes. Since many small-and-medium sized businesses are less familiar with such products, specialised providers offer expert guidance to help clients tailor their strategies to fit their specific goals and needs.

This combination of accessible tools and personalised support allows businesses to manage currency exposure and protect their profit margins, giving even smaller firms a strategic advantage.

Customer support: general vs. specialised

Cross-border transactions can be complex. When issues arise, quality support isn't just convenient—it's crucial.

With international payments, problems don't stick to business hours. They pop up in different time zones, speak multiple languages, and often need expert handling. Top-tier support means expertise in international finance and proactive guidance.

Traditional bank support

While banks typically offer support during business hours via phone, email, or in-person at branches, in practice, response times can be slow due to their size and complexity.

Additionally, unless you're a larger client, you may not have a dedicated point of contact who understands your business, and access to FX and currency payment specialists is often limited. This tiered support system often leaves small and medium-sized businesses feeling underserved.

Specialised provider support

Providers like iBanFirst that focus specifically on cross-border payments often offer a level of support that is tailored to the unique needs of businesses engaged in international transactions.

Specialised expertise: Unlike traditional banks, the support staff at specialised providers are experts in international payments and foreign exchange. This focused knowledge means they can offer in-depth support on complex issues related to cross-border transactions, currency risk management, and international banking regulations. For businesses, this translates to faster problem resolution and more informed decision-making.

Dedicated account managers: Some specialised providers like iBanFirst even go one step further and assign dedicated account managers to each business client, regardless of the company's size. This means that even SMBs can benefit from personalised service. These account managers develop a deep understanding of their clients' business models, payment patterns, and specific needs, allowing them to offer tailored guidance and solutions.

Proactive approach: Instead of waiting for clients to reach out with issues, specialised providers often take a proactive approach to support. This might include:

- Sending regular market updates and currency forecasts

- Alerting clients to favourable exchange rates

- Suggesting ways to optimise payment strategies based on analysis of the client's transaction patterns

- Providing information about regulatory changes that might affect the client's international payments

Faster response times: With a more focused service offering and often smaller client bases, specialised providers can typically offer faster response times. This is particularly beneficial when dealing with time-sensitive international transactions.

Specialised providers like iBanFirst aren't just moving money. They're empowering small and medium businesses to operate efficiently internationally with:

- Expert support tailored to your business

- Proactive guidance on payment strategies

- Personalised service, not generic call centres

The result?

- Slashed costs on international transfers

- Smoother cash flow across borders

- Smarter, more competitive global operations

Choosing the right option for your business

When weighing traditional banks against specialised providers like iBanFirst, consider:

Transaction profile

- Frequency: Several payments per month? Or just occasional?

- Volume: Are you moving millions or thousands?

- Currencies: Payments include both major and minor currencies?

High-frequency, high-volume businesses often benefit more from specialised providers' optimised systems.

Cost sensitivity

- Exchange rates: How much do small percentage differences impact your bottom line? How tight are your margins?

- Fee structures: Are you dealing with many small transfers or fewer large ones?

- Hidden costs: Have you calculated the true cost of your current solution?

Specialised providers typically offer more competitive rates and transparent fee structures, which can lead to significant savings over time.

Speed requirements

- Payment urgency: How fast do you need your payments to reach your beneficiary?

- Cash flow impact: How does payment speed affect your operations?

- Market opportunities: Could faster payments help you seize time-sensitive deals?

Specialised providers' streamlined processes could give you a competitive edge with faster payment processing.

Support needs

- Complexity: What’s your level of expertise when it comes to FX and international payments?

- Availability: Do you need support outside standard banking hours?

- Personalisation: Would dedicated account management benefit your business?

Specialised providers often offer more tailored, expert support for international transactions.

Technology and innovation

- Ease of use and accessibility: How crucial is having a user-friendly platform and real-time access to FX markets?

- Innovation appetite: How important are cutting-edge features like trackable payments or FX alerts?

Tech-forward businesses may find specialised providers' advanced platforms more aligned with their needs.

|

|

Traditional Banks |

iBanFirst |

|

Cost |

Higher exchange rates, less transparent pricing. |

Competitive exchange rates, reduced fees and transparent pricing structure. |

|

Speed |

Slower processing—can take from 2 to 5 days. |

Faster transfers—settle in 2 days or less. |

|

Support |

General customer service with limited availability and expertise. |

Dedicated account manager with expertise in international payments. |

|

Technology |

Outdated, clunky systems with limited capabilities. |

Powerful and intuitive platform with a wide range of specialised features designed specifically to streamline cross-border payments. |

The verdict:

For SMBs with frequent international transactions, complex needs, or growth ambitions, specialised providers like iBanFirst often provide a compelling package of cost savings, speed, expert support, and innovative tech.

However, businesses with simpler needs and less frequent cross-border transactions may find their current bank sufficient.

Ultimately, the right choice depends on your unique business profile, future plans, and how you prioritise these various factors.

Conclusion

Cross-border payments are a critical component of global business, and the choice between traditional banks and specialised providers can have significant implications for your operations. While traditional banks offer a wide range of services, specialised providers like iBanFirst have innovated to address many of the pain points associated with international transfers.

By offering more favourable exchange rates, faster processing times, specialised support, and advanced technological features, these providers are changing the landscape of cross-border payments.

As you evaluate your options, consider not just the immediate costs and benefits, but also how your chosen solution will support your business's growth and international expansion in the long term. The right cross-border payment solution can be a powerful tool in your global business strategy, enabling you to operate more efficiently and competitively in the international marketplace. Request your free iBanFirst account here.